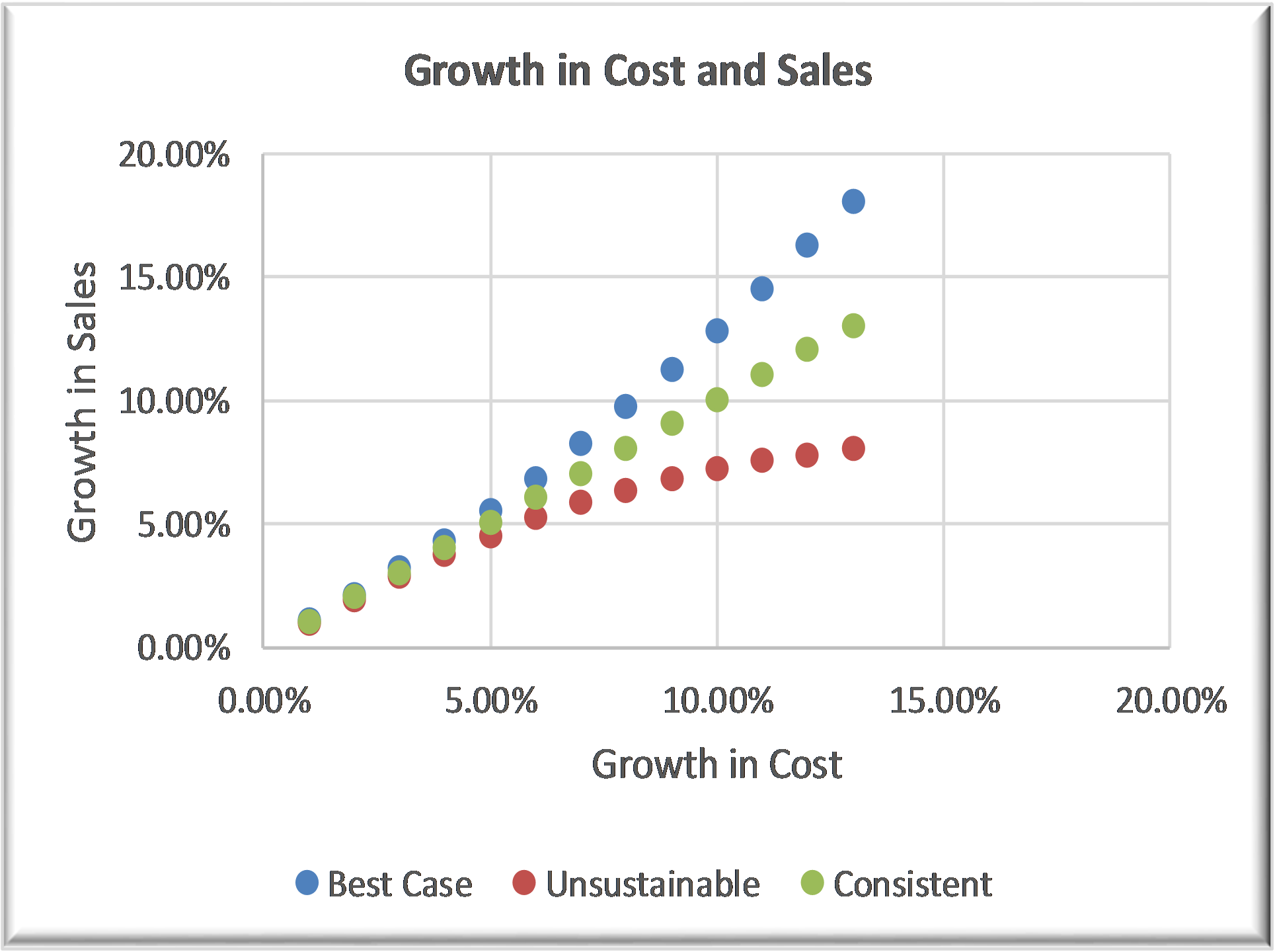

I consider managing cost to be as important as managing growth. Since costs are inputs for generating sales, we expect them to grow slower than sales. Only then the profitability, as measured by the margin on sales, will go up. In other words, we expect growth in sales to be better than growth in cost – a situation presented as the best case situation in the chart below.

If not, we must have a strong reason (e.g., a regulatory requirement) or a physical constraint (existing design limitation) that is coming in the way of managing costs or growing sales. A physical constraint can, of course, be removed by innovation, which may include investment in product or process design.

We do have situations where a leadership team may focus on growth for a short period, without investing an equal amount of effort in managing costs. Such an approach may not hurt the firm, as long as the leadership team is aware that this is a temporary imbalance in allocation of effort and they plan to come back to managing cost in a time-bound manner – sooner than later.

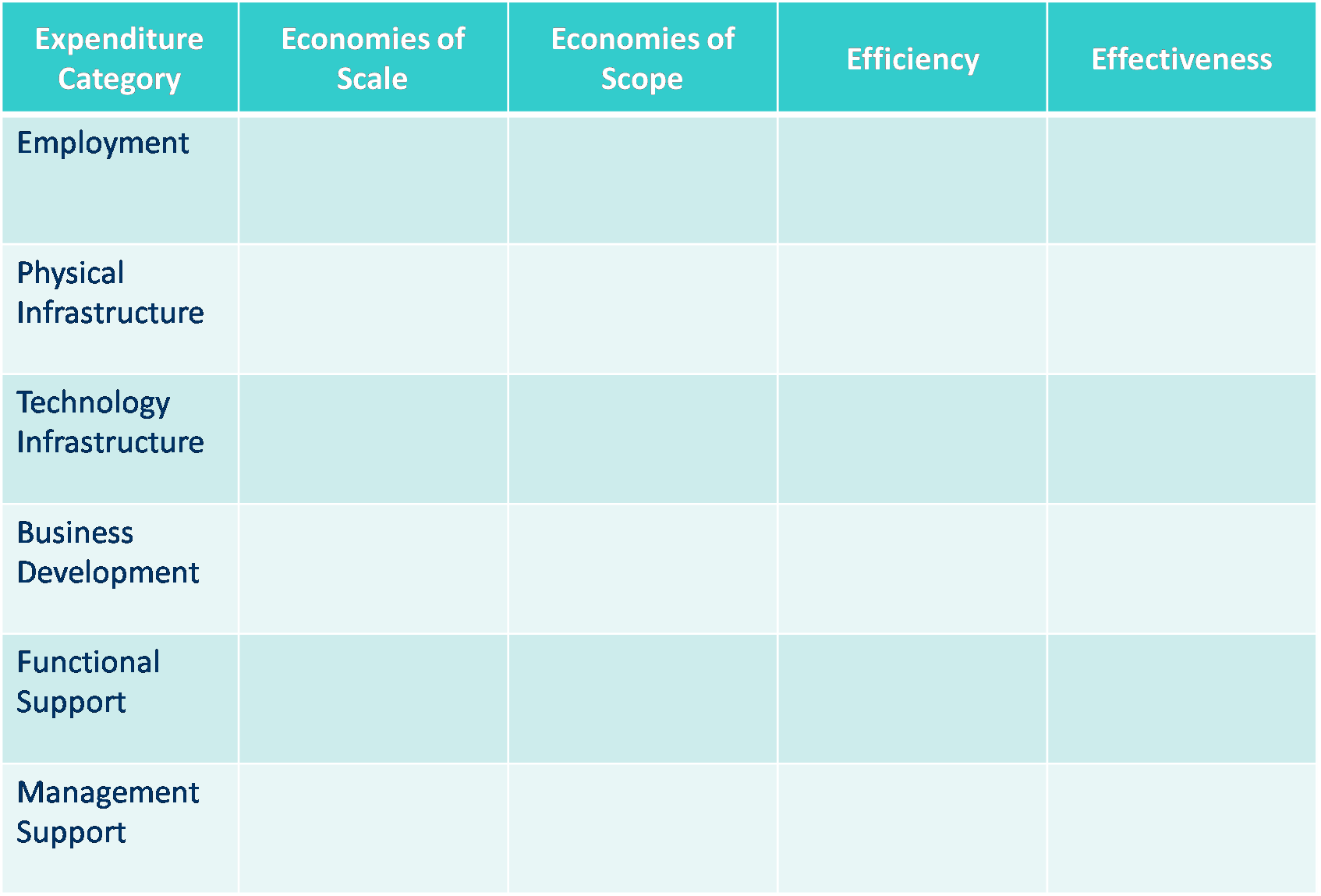

My note below presents a comprehensive framework that can help understand how our choices impact the structure, level and behaviour of different costs. The framework is also expected to help manage costs, as we track our progress on realising economies of scale and scope, driving efficiency and managing effectiveness.

In addition, I have presented a few core ideas that can help bring design focus to cost management.

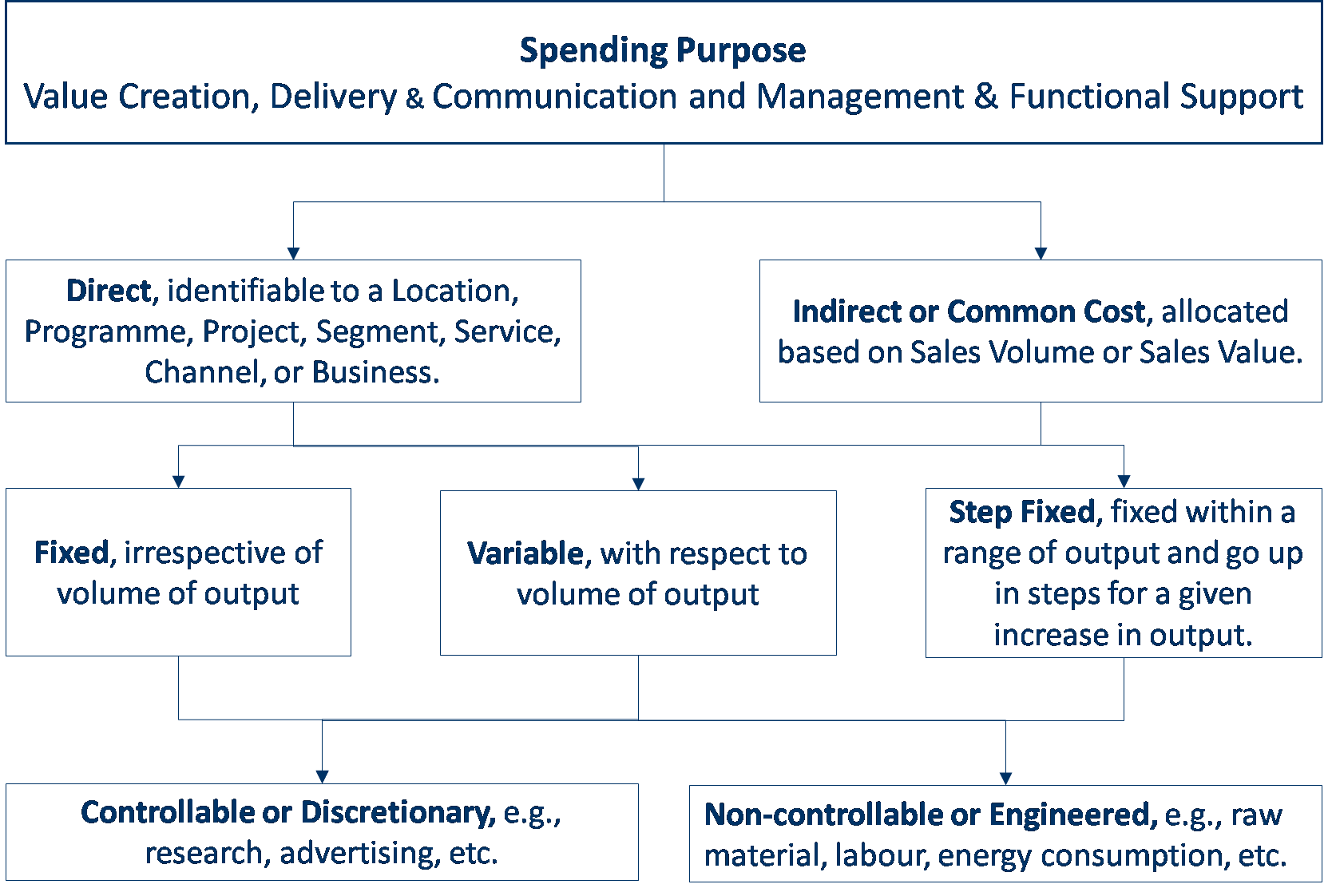

Understanding the Cost Structure

As a first step, we need to understand the cost classification so that we can understand how each cost type is expected to behave. Cost classification also helps us identify the cost drivers. For example, we know that a variable cost will vary directly in proportion to the volume, implying that volume is its driver. Similarly, location will be the driver of a cost that is directly identifiable with the location, i.e., higher the number of locations we operate from, higher will be the cost or the cost will vary with each location depending on the cost of living for that location.

Cost classification also helps us gain insights about managing costs. An engineered cost can be managed only through design changes guided by value engineering ideas. For example, if we want to reduce raw material cost, we will need to change the design to reduce the quantity of material or the kind of material to be used.

Cost Management Framework

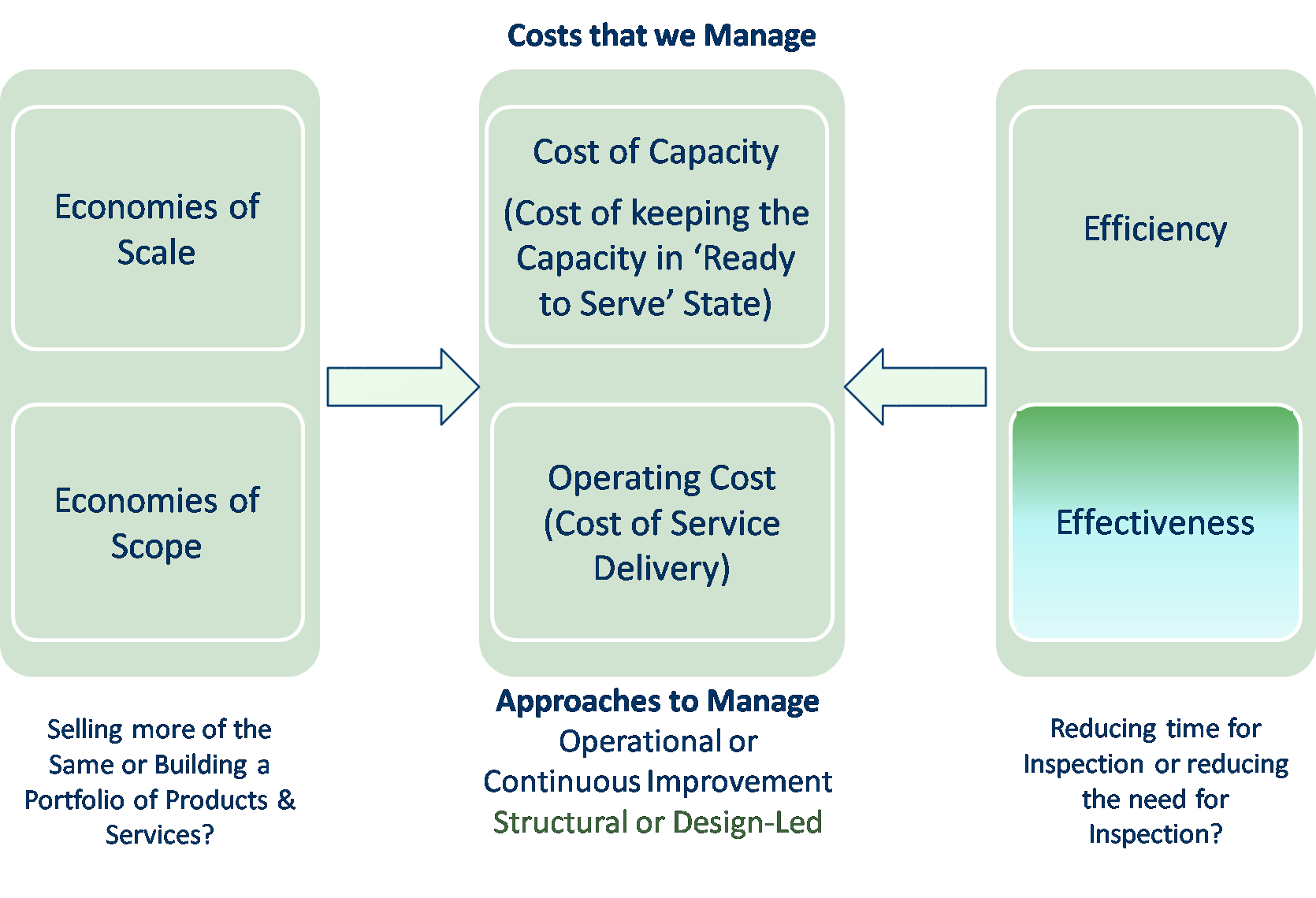

The cost management framework below presents the broad approaches and the costs that need to be managed. I have used the idea of ‘cost of capacity’ to classify costs. Cost of capacity includes all the costs that must be incurred even before we start serving our clients. Cost of capacity is particularly important for a business that has high fixed or committed costs. For example, a bank or an information technology firm needs to invest large sums in technology and physical infrastructure and hiring people even before they sign up their first client. However, we can use outsourcing as a way to covert our cost of capacity into cost of service or variable cost.

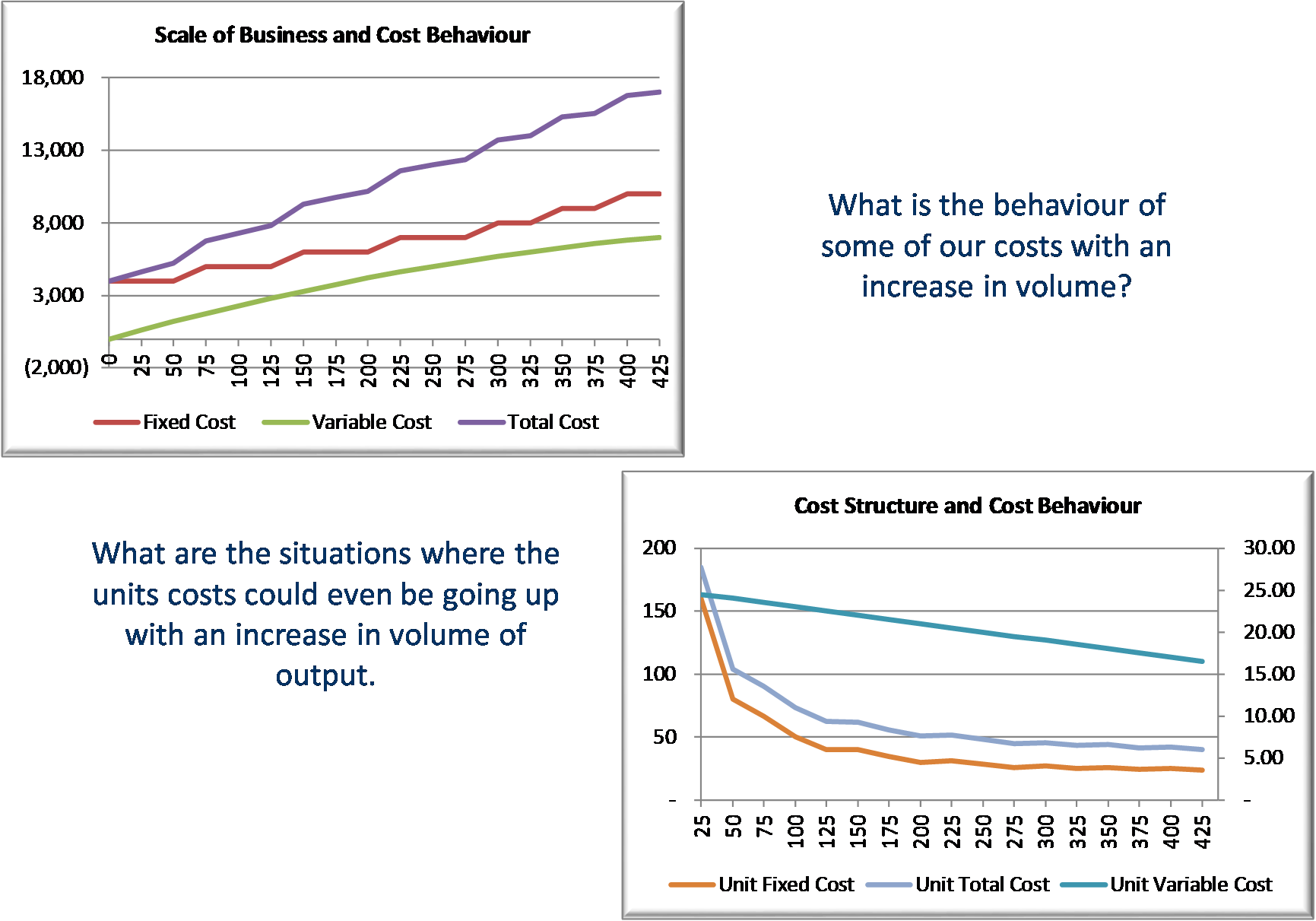

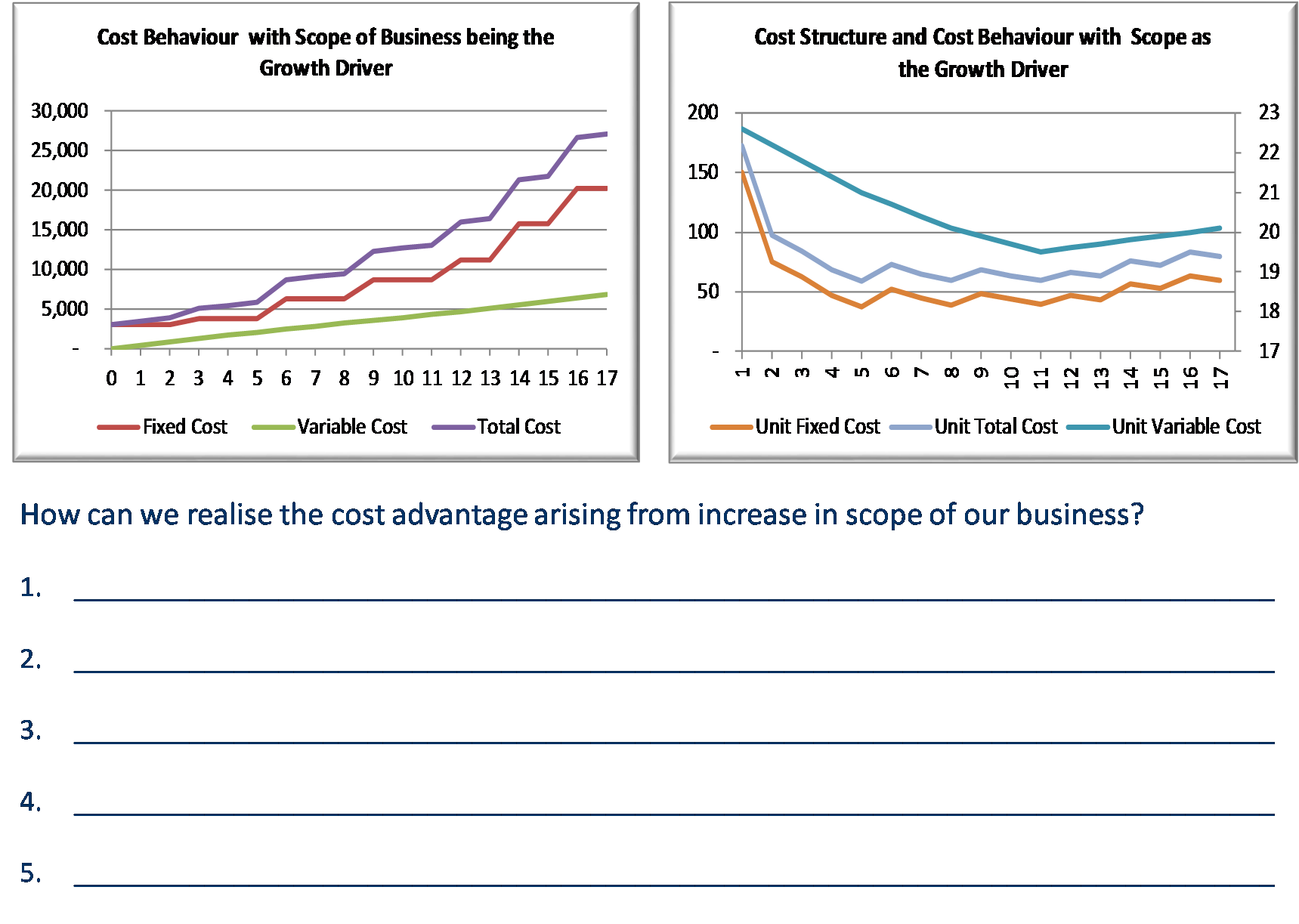

Economies of Scale and Scope

The next two charts present stylised cases of volume-cost and scope-cost relationships.

Cost Behaviour, given Economies of Scale

Cost Behaviour, given Economies of Scope

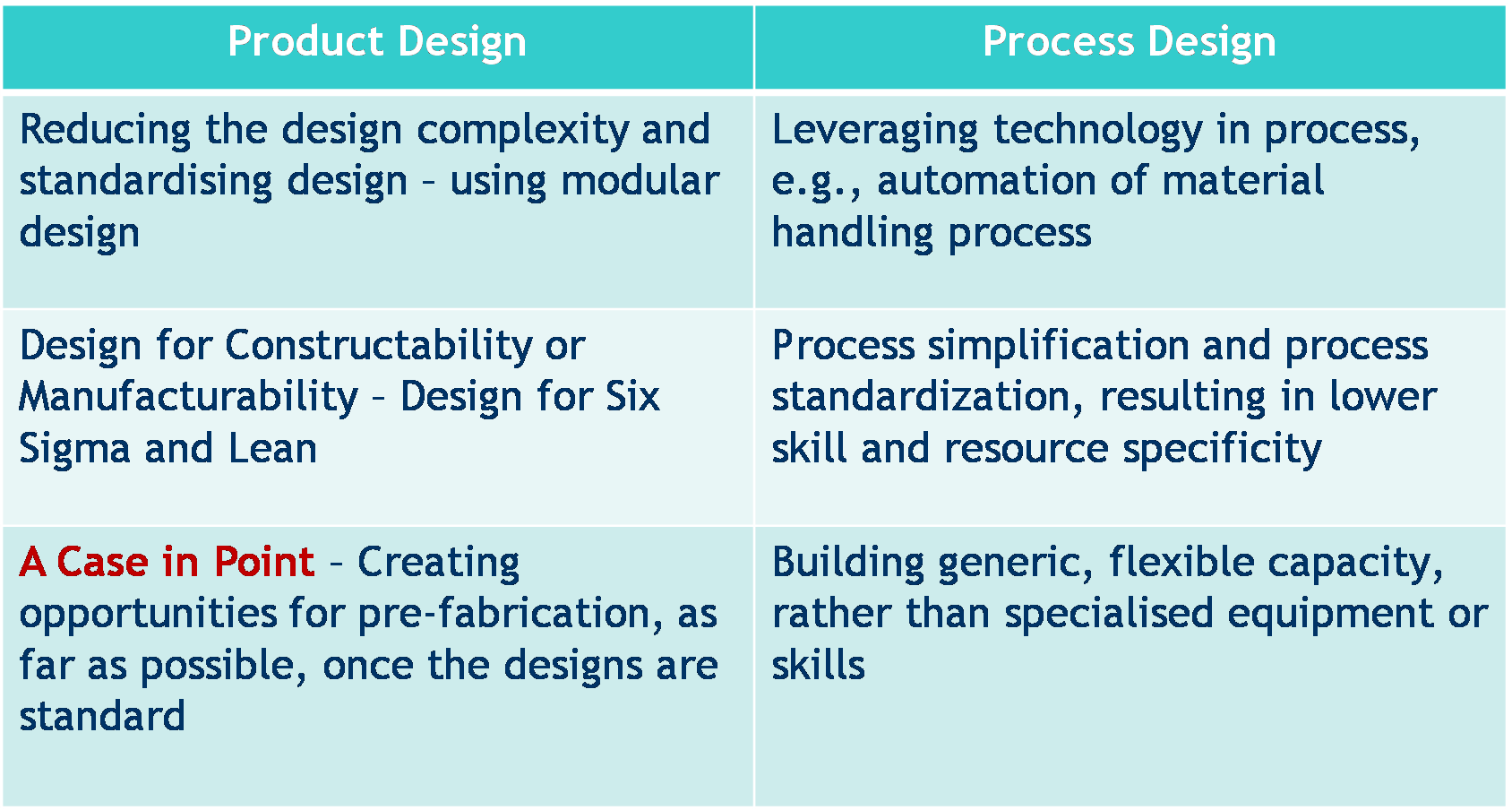

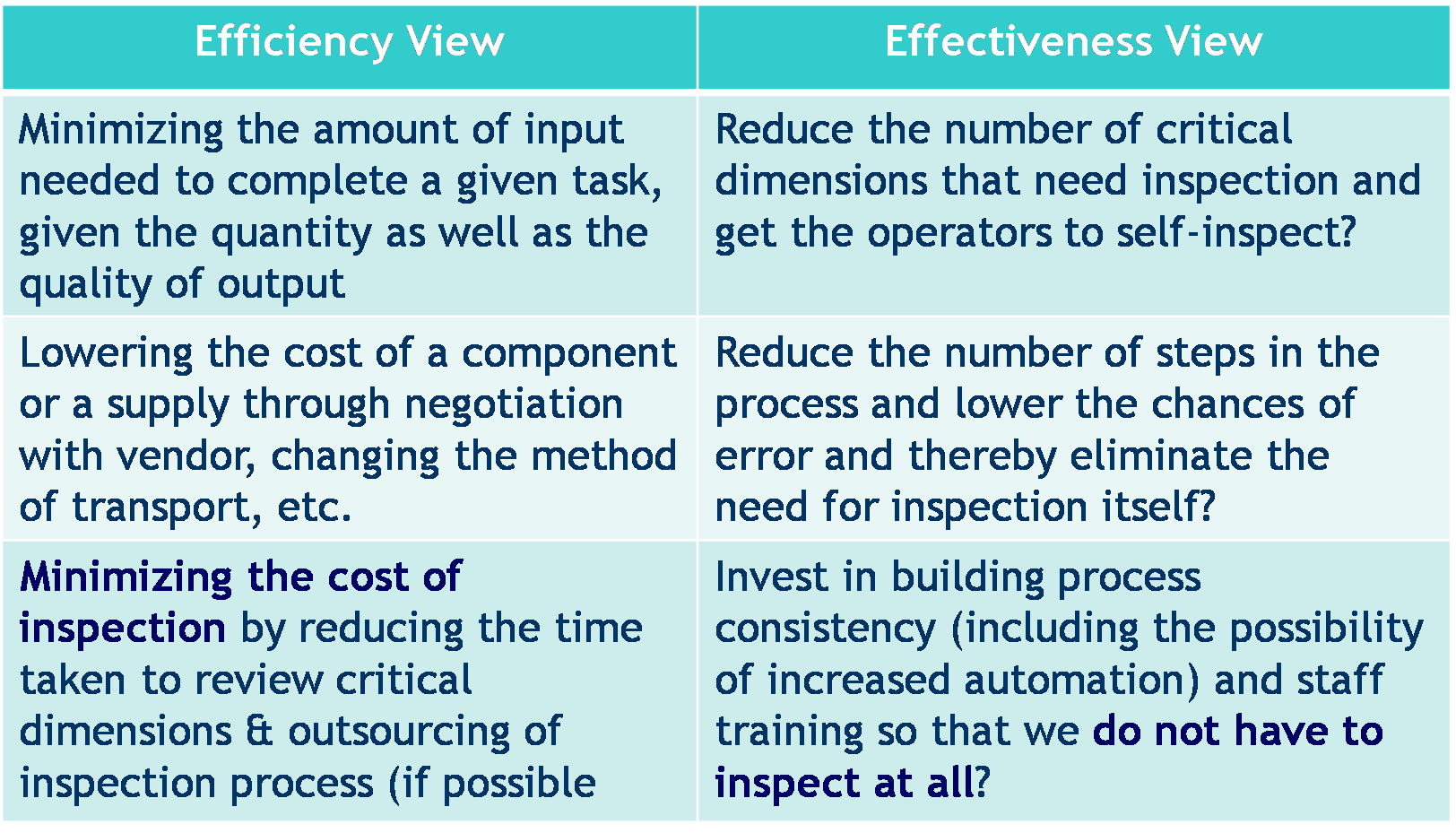

Structural Cost Advantage through Design… comes from

Doing things right and Doing the right things!

Self-Reflection and Application to Context