Farmers & Existing Agri-chain Players: Strategic Options under Changing Agriculture Landscape

Prologue

In a free market economy theoretically, price is determined by demand-supply situation, but in reality, the story is slightly different. Let us take an example, demand of a particular commodity ‘X’ is 5 million ton and supply is enough to meet the demand. Commodity ‘X’ is priced at INR 15000 (USD[1] 200) per ton. On an average its delivered cost and cash[2] cost of production are INR 10,500 (USD 140) and INR 6000 (USD 80) per ton respectively. Suppose in a year supply exceeds demand by just 10% (i.e., by 0.5 million ton), what will be the price of commodity ‘X’? Will it be down by 10% or more? And how far the price can go down?

In the above case, the price of commodity ‘X’ will be determined by that additional 10% supply which is freely tradable[3]. And price can go down to the level of INR 9000 (USD 120 = Cash Cost 80 + Avg. Cost of delivery 40) per ton. That is the drop of 40% in price, i.e. just 10% additional supply is knocking off price by 40%. If price goes further below, some plants which have cash cost of production at INR 6000 (USD 80) per ton would get shut and markets would settle down according to the new dynamics.

In-order to have some influence on the price of commodity ‘X’, it becomes necessary to have some kind of control over that 10% surplus quantity. And probably that is the reason corporates worldwide try various strategic options to have some kind of control over that 10% surplus quantity, which is freely available for the trade.

Now replace commodity ‘X’ with an agricultural commodity. In the case of agricultural commodity, producers[4] don’t have the option to shut production as most of them are doing farming for their survival and they don’t have any other revenue stream to support expenditures. Therefore, for agricultural commodity ‘X’, price can go down to any level. There is no support for the price at any level and probably that is the reason often farmers’ either throw their produce on the road or burn in the field.

Similarly, if there is a 10% shortfall in supply, the price of commodity ‘X’ can go up by more than 10%. But in the case of agricultural commodity, to protect households, government intervenes to moderate the price rise through export restrictions and easing imports. Therefore, for a farmer though upside gets capped, there is no floor/bottom on downside.

Government announces the ‘Minimum Support Price’ (MSP) for 22 mandated crops and ‘Fair & Remunerative Price’ (FRP) for Sugarcane, but in the absence of buying support, MSPs are meaningless and most of the crops are traded at much below the declared MSPs. Therefore, it can be said that MSPs do not work as floor/bottom. And, probably that is the reason farmers are demanding to make MSPs legally binding i.e. below that any purchase activity should not take place.

Recently introduced 3 farm acts[5] are going to affect the economic landscape of agriculture. Proposed changes will not only affect farmers but also the entire agri-chain, which includes Middlemen[6], Traders[7], Mandis, Warehouse operations, Dal mills, Rice mills, Sugar mills, etc. Under the changing landscape how farmers could chalk out their response to increase their bargaining power? This note discusses various such strategic options using a 2×2 matrix – ‘Farmers’ control on Production’, on one axis & ‘Farmers’ control on Supply’ on another axis.

Changing economic landscape of Agriculture

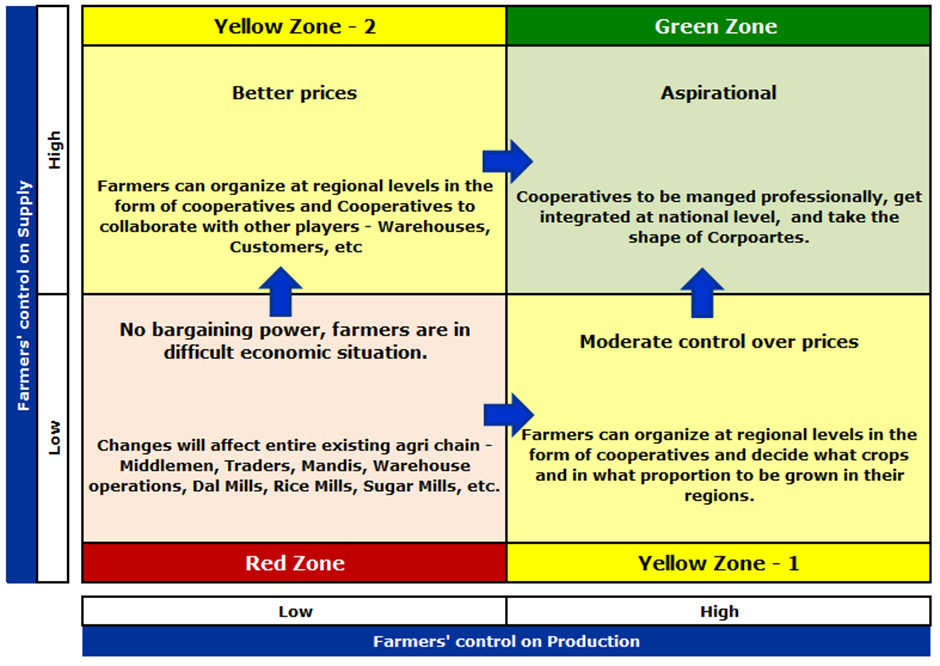

Two factors – control over production and supply, would be the key factors in agriculture space in the time to come, which not only help in fair discovery of price but also increase bargaining power of the farmers. To take the discussion forward we have used the following 2×2 matrix which has 4 quadrants – Red Zone, Yellow Zone-1, Yellow Zone-2, & Green Zone.

Red Zone: No bargaining power, farmers are in difficult economic situation

(Low ‘Farmers’ control on Production’ & Low ‘Farmers’ control on Supply’)

This quadrant represents the present condition of Indian farmers. As discussed in above paras, farmers don’t have any control over production, i.e., they don’t regulate farm outputs. So, when a crop is good i.e., at the time of better output, price crashes and farmers get negatively hit.

Agriculture is a seasonal activity, a crop is harvested simultaneously in many regions and is stored for regular consumption till the next crop comes. It is observed that prices at the time of harvesting are significantly lower than what consumers pay in subsequent months. As farmers’ don’t have control over storage facilities as well, they fail to capture the value out of storage activities – storing the crop and slowly releasing it into the markets at better prices for consumption. Imports are part of the supply only, which are also not in the hands of farmers.

Under the given circumstances how could 3 farm acts help improve the situation? Indian agriculture is facing the problem of surplus, except in few crops viz. Dalhan (pulses) and Tilhan (oil seeds). In the surplus situation how creating more traders and trading platforms for marketing[8] would help farmers to get better prices?

As ‘The Essential Commodities Act’ is modified and other 2 farm acts support private participation, one can argue that now large organised players with big storage facilities would directly participate in buying the farm outputs and hence farmers could expect to get better prices. That is a fair assumption to make, but it seems farmers are not having trust in organised players despite the fact that already, private traders and private trading platforms are active in the markets of various states.

If not private players, what is the alternative? I think the only alternative left under ‘Red Zone’ is that government should increase the buying and make MSPs legally binding. But, considering the size of agriculture and surplus situation, government buying will not provide necessary support, plus it is also not practically feasible. And, if MSPs[9] are made legally binding, private players would cut their role in the agri-chain, and the situation will become worse for the farmers.

Yellow Zone-1: Moderate control over prices

(High ‘Farmers’ control on Production’ & Low ‘Farmers’ control on Supply’)

In this zone farmers have control over production but have low control over supply. In normal time this situation arises when part of a crop gets damaged due to weather or some other reasons in a particular region. Due to the crop damage, shortage gets created and prices go up, which ultimately benefits farmers. But when prices go beyond certain levels, government intervenes and prices get softened. Therefore, benefits to the farmers get limited.

Contract farming where purchase is assured at predefined prices could help farmers to increase their income. Small and marginal farmers who are 86% of total farmers could get benefitted with the scheme of aggregation and contract. Contract farming is not something new, it is already in the practice. But, experience at this front has been mixed so far. Contracting firms rather than creating necessary infrastructure for storage, use existing infrastructure and hence other farmers lose out the access of those available facilities for storage. In the process the price of that particular commodity goes down affecting other farmers immediately and contract prices in the next cycle. It is expected that new acts would help create such infrastructures, which would ultimately benefit the trade in the long run.

If not private players, what is the alternative? I think one alternative under ‘Yellow Zone-1’ is that farmers should come together and form regional cooperatives. These regional cooperatives should interact with each other at national level and decide what crops should be grown and in what proportion in their regions keeping demand and supply situation in mind. For example there is a clear cut case to reduce the production of Wheat, Paddy, and Sugarcane at national level. How to achieve balance among various crops can be discussed and decided by regional cooperatives. That is the only way to exercise control over production and ensure that farmers get better prices.

Yellow Zone-2: Better prices

(Low ‘Farmers’ control on Production’ & High ‘Farmers’ control on Supply’)

In this zone farmers have low control over production, but have high control over supply. This situation can arise when adequate storage facilities are available at reasonable cost to the farmers. But, who will create such storage infrastructures? Ideally that is the job of governments- Central and States, but both have not been successful in creating such infrastructures and it seems that in future also governments will not do much at this front.

Private participations in creating such infrastructures have been muted so far as private players may not be seeing enough value in creating such standalone infrastructures without having forward – buying, and backward – selling, linkages. 3 farm acts provide basis for such linkages and encourage private participations in creating necessary infrastructures.

If not private players, what is the alternative? I think the only alternative is that farmers should come together and create cooperatives and those cooperatives should invest in such infrastructures. But, required investment is huge and it would be really tough for the cooperatives to raise funds. Alternative to raising funds directly is to collaborate with other existing players. 3 farm acts are going to affect the operations of warehouses, cooperatives can tie-up with such warehouses and other processors viz. Dal mills, Rice mills, Sugar mills, etc to create control over supply and increase their bargaining power in the new system.

Green Zone: Aspirational

(High ‘Farmers’ control on Production’ & High ‘Farmers’ control on Supply’)

In this zone farmers have high control over both production and supply. This is the ideal zone and it must be the ideal destination for the farmers. But, how could farmers reach there? If 3 farm acts help in reaching there, farmers must embrace the change. And, if not they must study the alternatives. One of such alternatives could be to form regional farmers’ cooperatives and let those cooperatives decide what crops need to be grown in their region in order to have control over production. And, in order to have control over supply those cooperatives need to invest and collaborate with other existing players in creating necessary infrastructures viz. Storage, Mandis, etc. Cooperatives need to be managed professionally and those should function like corporates.

Whether 3 farm acts stay or go, farmers could think about forming regional and national cooperatives which will help them in increasing their bargaining power.

Conclusion

Changes are going to come, and agriculture space would also be opened up. In the process there would be agitations, delays etc, but changes will happen. And, changes are going to benefit farmers in the medium to long run. Farmers need to think about how they could increase their bargaining power under new systems. If they have bargaining power, all the changes and new systems will work in their favour. And, to increase bargaining power they must have certain economic control over production and supply through their own cooperatives which get managed professionally just like corporates.

Apart from farmers other existing players of the agri-chain also need to think on above lines.

[1] 1 USD = INR 75

[2] Cash cost = Total cost of production – Depreciation, depreciation is USD 20 per ton.

[3] Not taking into account other factors viz. commodity exchanges, low dollar index, excess liquidity, etc

[4] In Indian context

[5] 3 farm acts are – 1. The Farmers’ Produce Trade and Commerce (Promotion and Facilitation) Act; 2. The Farmers (Empowerment and Protection) Agreement of Price Assurance and Farm Services Act; and 3. The Essential Commodities (Amendment) Act

[6] People who buy from farmers.

[7] People who buy from middlemen.

[8] In agriculture Marketing and Trading are two separate activities. Farmers selling to traders are considered as marketing while traders selling further down the line are considered trading.

[9] MSPs are declared by Central, not by States, and the cost structures of states for a crop are different. MSPs are also influenced by political compulsions.